{kind=link}

{kind=link}

EN

-

Calibrate GARCH(1,1) model table

After we calibrate the GARCH(1,1) model, and verified its assumptions by examining the residuals, we are ready to use it for forec…

-

Selecting forecast icon in NumXL toolbar

After you select the top cell in GARCH(1,1) Model table, locate the forecast icon in NumXL toolbar (aka Tab), and click it to Invo…

-

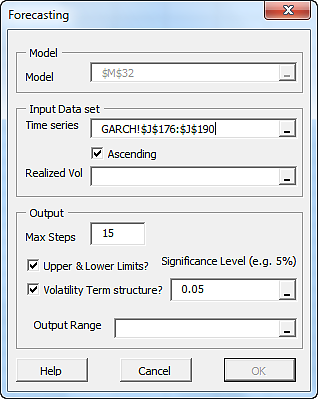

NumXL forecast wizard/dialog

The NumXL Forecast wizard/dialog pops up. The model reference cell is already selected and grayed out in the dialog.

-

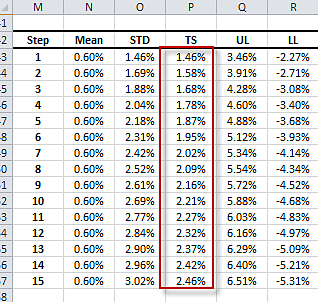

GARCH(1,1) Forecast table showing term structure volatility

In this GARCH(1,1) forecast table (generated by NumXL Forecast wizard), the volatility term structure forecast are shown in the re…

-

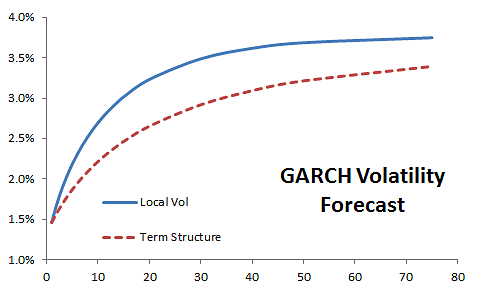

Plot for Local and term structure volatility forecast using GARCH model

In this plot, the local (aka forecast error) and term structure volatility forecast are plotted together. Note that both curve con…

-

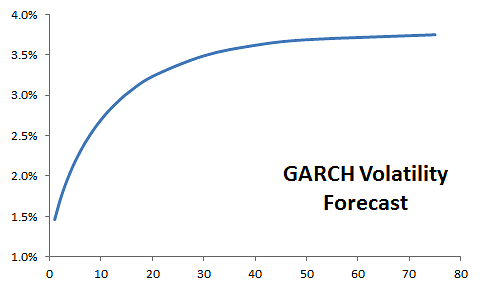

GARCH(1,1) Local olatility forecast for S&P 500 log monthly returns

In this plot, we show the local volatility (aka forecast standard error) over the forecast horizon. Note that volatility revert to…

-

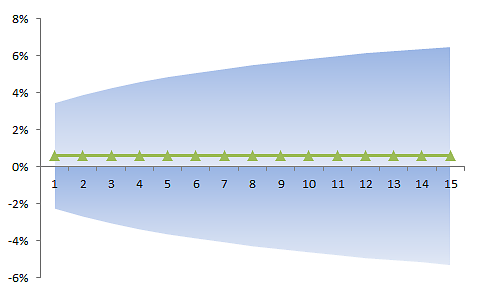

Plot for Forecast values and their confidence interval

In the plot, we have the mean forecast (line), and the 95% confidence interval represented by the shaded area.

-

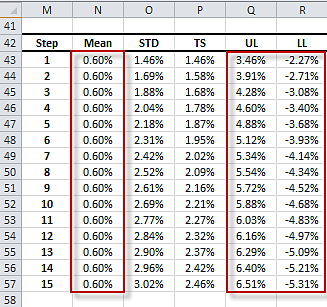

Forecast table for GARCH(1,1) model

he NumXL Forecast wizard generates a table with forecast value for the mean and Upper/Lower limits for the confidence interval. Th…