-

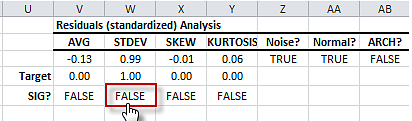

Residuals Diagnosis - Testing for standard deviation(i.e. sigma)

In the residuals diagnosis table, we perform a statistical test for the significance of the standardized residuals standard dev…

-

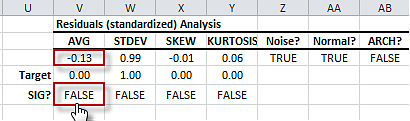

Residuals Diagnosis -Examine the mean of the residuals

In the residuals diagnosis table, we perform a statistical test for the significance of the standardized residuals mean against…

-

Residuals diagnosis section in GARCH Model table

In the generated GARCH model table, the rightmost section contains tests and check for the standardized residuals to verify the un…

-

GARCH(1,1) Model table with calibrated values

Upon solver successful completion, the optimal values of the GARCH(1,1) model are inserted in the table, and calculation referenci…

-

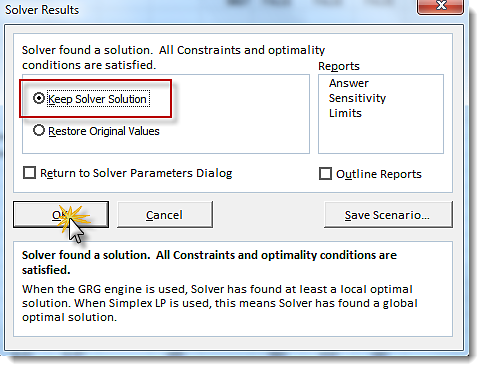

Excel Solver Found a Solution for GARCH(1,1) calibration

Excel Solver found a solution for the calibration problem of the GARCH Model

-

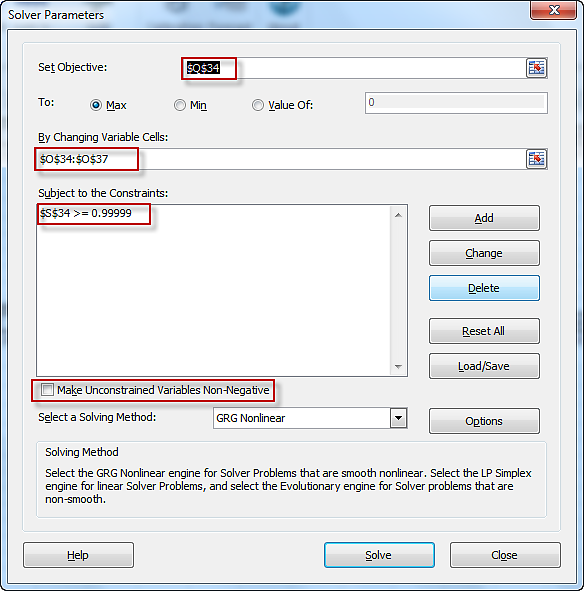

Excel Solver with GARCH(1,1) model calibration settings

NumXL launch Excel Solver with its fields initialized with model's cells: parameters, utility function (i.e. LLF) and the constrai…

-

Selecting the calibration icon in NumXL toolbar

Select the header cell of the model table, Locate the calibration icon in NumXL Toolbar (aka Tab), in the Power Tools section, and…

-

GARCH(1,1) - Model stability check

In the middle part of GARCH(1,1) model table (aka Goodness of fit), note the formula under the CHECK. The function GARCH_CHECK ref…

-

Generated Formulas in the Residual Diagnosis section of GARCH model table.

The Residuals diagnosis section of GARCH(1,1) model table is dynamic; note the generated formula references the input cells range…

-

Generated formulas in the GARCH(1,1) model table

The generated GARCH(1,1) model table is dynamic; note that cells are populated with formulas the references model's parameters cel…

-

GARCH(1,1) Model table

The GARCH(1,1) model output table generated by NumXL GARCH wizard for the S&P 500 ETF log monthly returns time series.

-

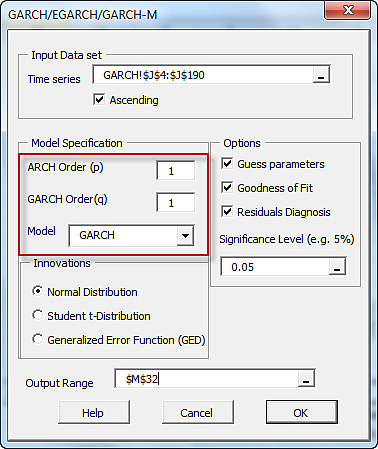

NumXL ARCH/GARCH Wizard

In the NumXL GARCH model wizard, enter the orders of the ARCH and the GARCH components. Leave Model selection to as GARCH

-

Selecting GARCH Wizard in NumXL Tab

Locate the GARCH icon in NumXL Toolbar (aka Tab), and click it to invoke the ARCH/GARCH Wizard.

-

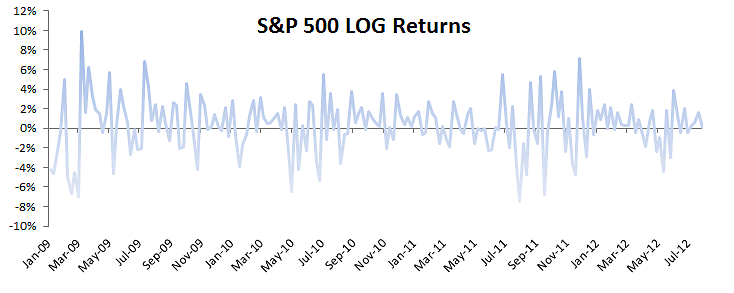

Plot for S&P 500 monthly log returns

A plot for the S&P 500 ETF log monthly returns between Jan 2009 and July 2012

-

The summary statistics table showing ARCH effect test

ARCH Effect test results for S&P 500 monthly log returns

-

Correlogram plot for S&P 500 squared log monthly returns

Correlogram or ACF and PACF plot for the S&P 500 squared log monthly returns

-

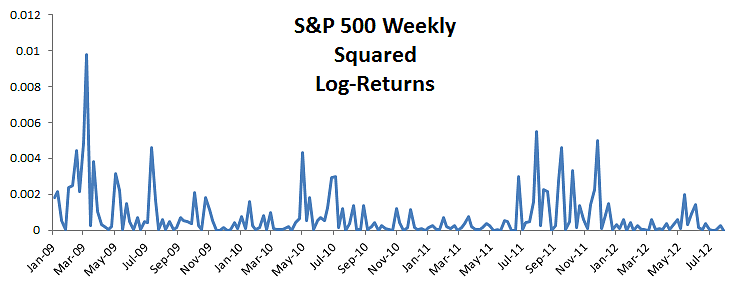

Plot for the S&P 500 squared monthly log returns.

Plot for the S&P 500 squared monthly log returns.

-

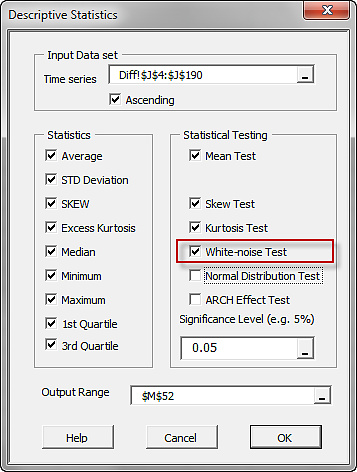

Select white-noise test in NumXL Descriptive Statistics wizard.

selecting a white-noise test in NumXL descriptive statistics wizard or dialog box.

-

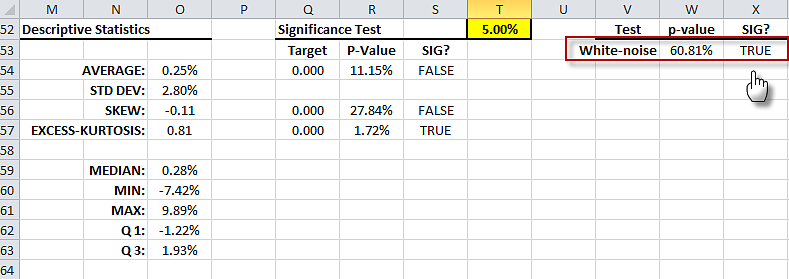

Summary Statistics table for S&P 500 monthly log return

Summary Statistics output table for S&P 500 monthly log returns with highlighted white-noise test.

-

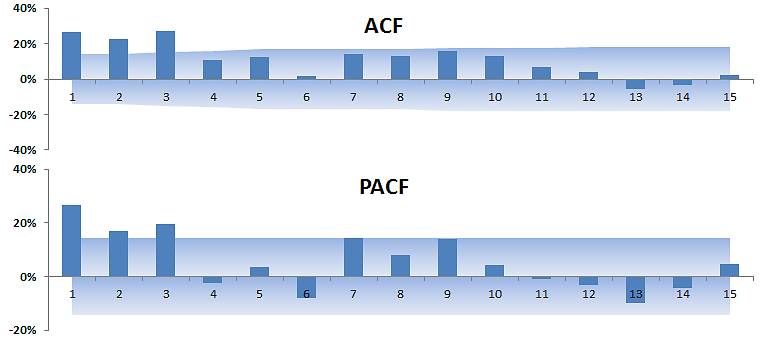

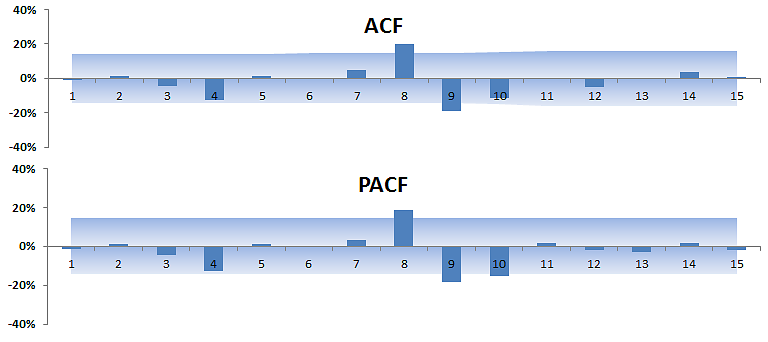

Correlogram plot for S&P 500 monthly log returns

The Correlogram or ACF & PACF plot for S&P 500 monthly log returns. (Generated by NumXL correlogram wizard)

-

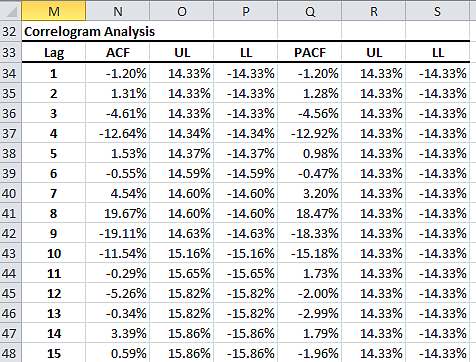

Correlogram table for S&P 500 monthly log returns

Correlogram output table for the S&P 500 monthly log returns.